Your Renewal Letter Is Coming. You Do Not Have to Sign What the Bank Mailed You.

The renewal letter is on the counter. You have read it three times. The new payment is hundreds of dollars higher than the one you have been making for five years, and your stomach has not settled since it came in the mail.

We get it. You locked in back when rates were near the floor. Life made sense at that payment. Now the bank wants to renew you at a number that feels like a different planet, and nobody asked whether your grocery bill or your kid's fastball season got any cheaper in the meantime. (They did not.)

Here is the part most families do not hear in time. That letter is an offer, not a verdict. And the right move can take a couple hundred dollars a month back off that payment, starting the month you renew. Not someday. This renewal.

Here is what that looks like

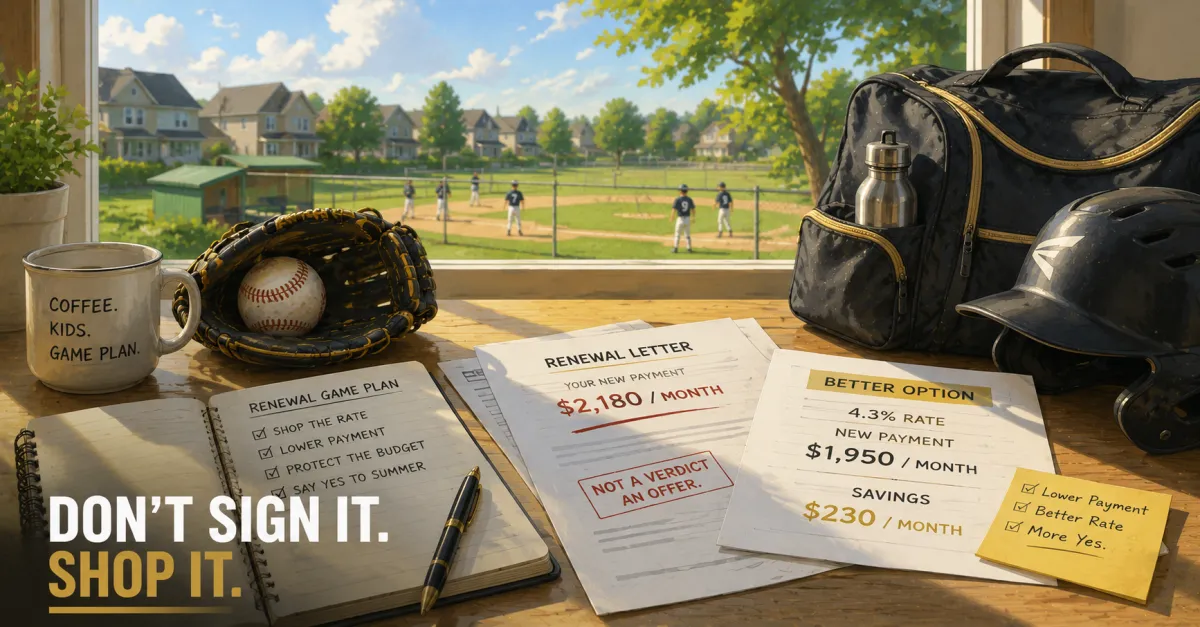

A fastball family came to me this spring with a renewal letter just like yours. Two kids in the summer travel circuit, a garage full of bat bags, and a mortgage of about $360,000 left on the house.

Their old rate was 1.9 percent. The payment they had gotten used to was around $1,510. The bank's renewal offer came in at 5.4 percent, which pushed the new payment to roughly $2,180. That is $670 more a month for the exact same house. Same roof. Same kitchen. Same kids.

Most families would have signed it. It is the easy thing to do when you are tired and the letter has a deadline on it.

We shopped it instead. We moved them to a lender at 4.3 percent and restructured the amortization so the new payment landed around $1,950.

Still higher than the old payment, because rates are higher now and there is no magic in that. But $230 a month lighter than what the bank wanted. And $230 a month is the difference between a summer you brace for and a summer where the tournament travel is just handled.

What I told them next

The rate on the renewal letter is not the rate you are stuck with. The Bank of Canada is holding its key rate around 2.25 percent and meets again on June 10, but your renewal rate is set off the bond market and your lender's appetite, not just the headline everyone talks about. That means the number in the envelope is a starting point, not the final word.

Coaching my own kids was the best part of my life. I never wanted the bank's calendar to decide whether a family got their season. The renewal wall does not care about your summer. My job is to make sure your mortgage does.

And once your renewal is sorted, we keep planning together. I bring in the partners I work with, the people who help families like ours grow and protect what we have built and pass it on to the kids one day. The renewal is the moment we meet. The relationship is everything after it.

I am not here for one signature. I am here for the next 30 years.

If your renewal letter made your stomach drop, do not sign it yet.

Five minutes at www.adamwalkermortgages.com/payment-shock-protection will show you what your renewal could actually look like. No email gate. No sales call. Just your real numbers.